Overview

Although the Azerbaijani economy has shown signs of recovery, the recession has continued in 2017. There were extensive reform initiatives on a number of issues, fundamental vulnerabilities of the economy still persist. Recovery process was not as much the outcome of adjustment to lower oil price levels, as much the result of the relative increase in oil prices. Despite diversification attempts, extension of the “Contract of the Century” and developments in Southern Gas Corridor project attest to the fact that oil and gas sectors will hold a central role in the economy of Azerbaijan in the foreseeable future.

Domestic demand has been among the main drivers of economic growth in the country in 2017. That is to say, real final consumption expenditure rose by 6.1% (20.8% in nominal terms) during the first nine months of 2017 compared with the corresponding period of the previous year. Nominal final consumption expenditure constituted nearly 86% of household income, while only 3.9% was saved. In order to meet an increasing consumer demand, there was an expansion in the volume of goods and services by 1.9% during the period. Retail trade turnover also demonstrated an increase of 2.1% reaching 12.2 billion manat. The share of the consumer funds directed to the purchase of food, drinks and tobacco products accounted for 50.6% of their total purchases through retail trade. The second largest share was recorded by textile products, clothes and shoes with 18.1%.

Growth in consumer demand was principally supported by a rise (8% during January-September 2017) in nominal income, as per capita monetary income growth constituted 6.9% and disposable income rose by 11.5%. Furthermore, nominal monthly average wage grew by 7.4% reaching 524.7 manat in January-August 2017 compared with the same period of preceding year. It should be stated that, growing consumer demand was not supported by an increasing access to credit, in fact, there was a significant decline of 16.7% in household loans in January-September 2017.

Government expenditure has been among the key drivers of domestic demand throughout 2017. Based on the data by the Ministry of Finance of the Republic of Azerbaijan state budget spending amounted to 12.8 billion manat. Notably, the share of social spending accounted for 38.1% of total budget expenditure exceeding the previous year’s indicator by 7.8% (or by 351.4 million manats).

On the other hand, investment expenditure decreased by 1% falling to 11.1 billion manats in the first nine months of 2017 compared with the same period of 2016. Oil and gas sector investments (58.5%) dominated the non-oil investments (41.5%) during the period. Private sector investments constituted 68%, while public sector accounted for 32%. Moreover, fixed capital investments were mainly financed by external sources (almost 60%). During the period, enterprise and organization funds (67.5%) represented the dominant share of total fixed capital investments.

The Extractive Industries Transparency Initiative (EITI) suspended the membership of Azerbaijan on March 9, 2017 during its 36th Board Meeting. Subsequently, the government of Azerbaijan decided to withdraw from the EITI, making an official statement that, the suspension decision was unfair, since the government made necessary changes to NGO regulations that was required the EITI[1] (Azernews.az, 2017). EITI is comprehensive standard to encourage the open and accountable management of oil, gas and mineral resources[2] (EITI). Currently, EITI has 51 implementing countries and it is supported by a coalition of government, corporations and civil society.

There are several important potential outcomes of Azerbaijan’s quitting the EITI. First of all, as a member of EITI, Azerbaijan used to comply with transparency and sustainable development principles and this made the country attractive for foreign investment and international financial institutions. British Petroleum, one of the major transnational companies operating in Azerbaijan, has already expressed its discontent with the situation[3]. Moreover, the stakeholders of the Southern Gas Corridor may also refrain from the project, as withdrawal from the EITI undermines the reputation of the country. This suspension may also adversely affect the civil society environment in Azerbaijan in the future, although the recent dynamics of EU-Azerbaijan relations demonstrates that, these undesirable effects can be avoided[4]

However, as the relatively timid reaction of BP has demonstrated, the main partners of Azerbaijan were not fazed by this development. As was already mentioned above, in September Azerbaijan have extended “Contract of the Century” which significantly improved conditions compared to initial contract. According to the new production sharing agreement, share of State Oil Company of the Republic of Azerbaijan (SOCAR) has increased from 11.65% to 25%. Furthermore, government will receive USD 3.6bn bonus over the next 8 years[5].

IMF statement issued on 15th of December have noted the positive tendencies in macroeconomic conditions. The statement notes that: “Growth prospects are positive in the near term. With expanding public investment and social spending, the nonhydrocarbon sector is expected to increase by 4 percent in 2018.”[6]

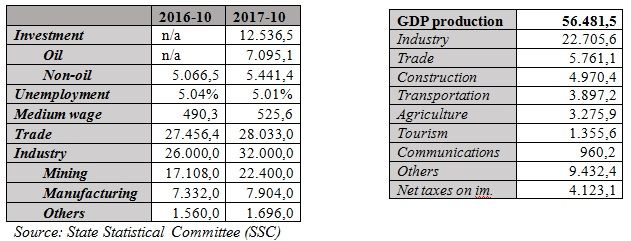

Table 1: Main Macroeconomic Indicators Table 2: GDP Components, 2017

State-Owned Enterprises

The SOEs encountered significant challenges following the devaluation of national currency. That is to say, majority of state-owned enterprises faced huge financial loss and their foreign debt levels almost doubled. Significant rise in debts of SOEs acquired with state guarantee necessitated a reform in this area. The president have approved rules for foreign borrowing of state-owned enterprises, determining upper limits of borrowing and the procedures that have to be followed. Moreover, the long-standing challenges concerning transparency and accountability are ever more pressing, as there have been inappropriate uses of allocated public funds. Some SOEs (such as Azerbaijan Airlines JSC, Azerbaijan Railways CJSC, “Aqrarkredit” Closed Joint Stock Non-Banking Credit Organization) operate under closed joint stock company principles that are entitled to monopoly position. Thereby, most of the SOEs create barriers for entry owing to their monopoly power in the market. The current situation of several major state-owned enterprises is analyzed below.

SOCAR is responsible for oil and gas extraction and processing. SOCAR is a sponsor of a number of local and international projects and currently experiences a considerable debt problem. For the purpose of an effective implementation of these projects SOCAR engages in credit and investment funding. The company has borrowed USD 1.4bn since the beginning of 2017[7]. The underlying reasons for a high debt include: overestimation of the performed work, the lack of high-level management specialists, the devaluation of the national currency, as well as the company's high taxation rate and social obligations to the population.

“Azerishiq” Open Joint Stock Company (electricity distribution company) has also faced a huge debt following the devaluation in 2015. Another issue worsening the financial situation of the company is mounting debt of the population to company. “Azerbaijan Railways” is considered one of the most vulnerable state companies in Azerbaijan. At the beginning of 2017 its debt amounted to USD 543m[8]. However, the company is expected to make profit in the future, as Baku-Tbilisi-Kars railway was finally completed and officially opened on October the 30th, 2017. Relatively more efficient SOEs include Port of Baku, AzerCosmos (satellite operating company) and Caspian Shipping Company.

Balance of Payments

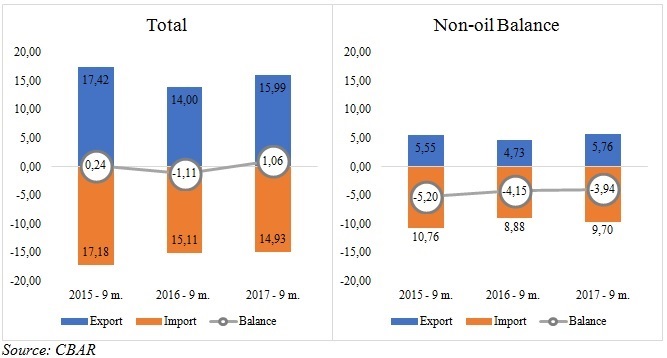

After 9 years of huge current account surpluses (which averaged at 23% of GDP), oil price slump beginning in 2014 have significantly reduced export volume of Azerbaijan, resulting in 2 consecutive years of current account deficit in 2015 and 2016 (-0.4% and -3.6% respectively)[9]. In all these years preceding the crisis, Azerbaijan have failed to diversify its export industry. The share oil and gas in exports have remained above 90%. The influx of oil revenue has facilitated of the expansion of non-tradable sectors (construction, financial services etc.), non-oil tradable sectors did not develop adequately.

The economic theory predicts the improvement of current account balance after depreciation of national currency, but we see the reverse in Azerbaijan, as current account deficit increased in 2016. Although two episodes of devaluation in 2015 should have theoretically give rise to import-substituting domestic industries and decreased the volume of imports, import of goods (in USD) was virtually unchanged from 2014 to 2015 and decreased only slightly from 2016 to 2017 (7.5%)[10].

The oil price has started to gradually recover in the second quarter of 2016. In January-November period of 2017, average daily price was 53.2 dollars, which was 23% higher than the corresponding period of 2016[11]. This has resulted in positive current account balance in the first three quarters of 2017. Current account balance in this period was USD 1bn., which is 3.6% of the GDP of the corresponding period[12]. We can expect this figure rise toward the end of the year, as the oil prices continued to rise in the fourth quarter.

Azerbaijan have been exploring the possibility of developing its largely untapped tourism potential in the past few years. Competition with Turkey, a globally known tourism powerhouse, did not favour Azerbaijan until recently, but depreciation of manat have significantly boosted the attractiveness of Azerbaijan for foreign tourists. There has been a significant influx of tourists to Azerbaijan in the past two years, especially from Gulf countries. The number of tourists visiting Azerbaijan in the first 11 months have increased by 25% relative to last year[13]. Total income from tourism in the first three quarters of 2017 have increased by 14.4% relative to 2016. The increase is even more significant when compared to 2015 – a 40% increase[14].

Figure 1: Current account balance –bn. USD.

Foreign direct investment (FDI) inflow have decreased significantly – 28.3% (2.4bn USD, around 8% of January-September GDP). The decrease was recorded both in oil and non-oil sector FDIs (1.6bn, 5% of GDP). It should also be noted that, FDI outflow have also decreased. Net FDI flow to country was USD 790m. Portfolio investment inflow have increased significantly – from 481m to 2763m[15].

Fiscal Policy

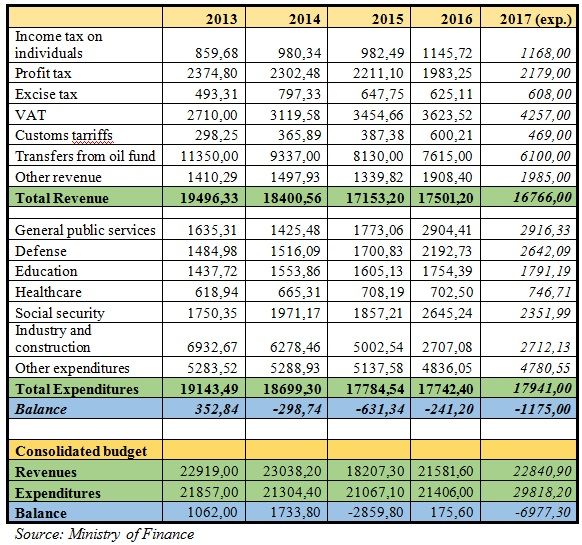

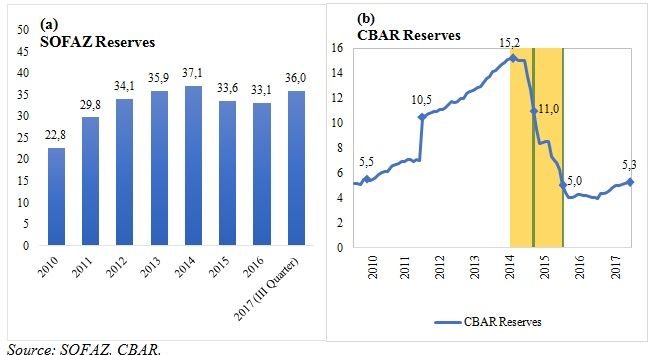

Even during the years of high oil prices, Azerbaijan have occasionally experienced budget deficit. Transfers from oil fund constituted a significant share of budget revenues. Despite these sizable transfers, oil fund reserves were consistently increasing prior to 2015. However, with dramatic decrease in oil prices, oil fund reserves have decreased in 2015 by USD 3.5bn, from 37.1bn to 33.6bn[16]. This decrease was unprecedented and it further highlighted the significance of diversification of economy. The heavy reliance of the budget on oil fund transfers was evident before, but wasn’t as strongly felt as in 2015. In 2016, it further decreased to USD 33.1bn. These developments have highlighted the need for fiscal consolidation in Azerbaijan. We should note that, with the increase in oil prices, oil fund reserves have increased by 8.67% in the first three quarters of 2017 and have now reached 36bn USD, which is its highest level since 2014[17].

Although the total budget revenues have decreased both in 2016 and in 2017, the decrease in 2017 came from the reduction in transfers from oil fund. This was in line with a broader strategy of decreasing the dependence of budget on oil fund transfers, which is expected to be repeated in the following years. While transfers decreased by 1.5bn manats, total budget revenues decreased by only 0.8bn, which means that tax and tariff revenue increased approximately by 0.7bn[18]. This increase was mainly due to increased efficiency of State Customs Committee. So much so, despite decrease in imports due to exchange rate depreciation, increased efficiency and transparency, reduction in corruption have increased revenue of Customs Committee from 1.8bn in 2016 to 2.2bn in 2017[19].

Table 3: State budget

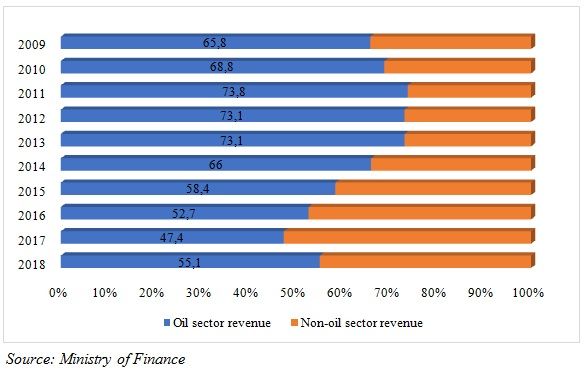

Main reforms on the revenue side include the application of electronic tax forms, simplification of customs regulation, expansion in the volume of cashless transactions. The government targets to modernize tax legislature to increase its rating in OECD Global Forum on Transparency and Exchange of Information for Tax Purposes. One of the critical issues facing the government is the deficit in social security system, which is 1.3bn AZN in 2017 budget plan. Although the revenues of State Social Security Fund have increased since 2016 (by 150m.), social security spending increase was larger – 320m., therefore, the deficit has increased. As stated by the Ministry of Finance, the share of oil-sector budget revenues has been in decline in the past years. For example, it fell from 54.8% to 49.2% from 2017, although this is in part due to decreased transfers from oil fund[20]. The reliance of the budget on oil is still significant, considering the indirect effects of oil prices through their effect on economic activity.

In the first 9 months, actual budget revenues have slightly exceeded the budget plan (by 0.2%). Tax revenue was 0.1% more than planned, while the revenue of Customs Committee was 17.9% higher. These developments have allowed the government to slightly decrease transfers from the oil fund – by 275m AZN (6%)[21].

Consolidation of budget spending have played a greater role in decreasing budget deficit. Budget spending in 2017 was planned to be 16.6bn manats, which is 1.9bn (10.2%) less than 2016. It should be noted that, not all components of public spending have been decreased. “General public services” spending has been increased by 17.8%, which was mainly driven by an increase in servicing of foreign public debt. Defence spending has also been increased significantly (43.7%) from 1.8bn to 2.6bn manats. Social spending, major component of which is social security spending, has been increased by 18.8%. Education and healthcare spending have remained roughly at the same level[22].

Figure 2: Share of oil and non-oil sectors in budget revenue

On the other hand, there is a significant decrease in the fuel and energy spending – from 5.6bn to 3.5bn manats, a 37.5% decrease. This was partly due to an increase in utility prices (natural gas and electricity). Furthermore, investment spending (part of “industry, construction and natural resources spending” in budget) have decreased by 1bn to 2.3bn manats in the past 2 years. In the first 9 months of 2017 actual public spending has exceeded the plan by 0.7%[23]. According to the latest revision to the budget of 2017, budget spending is set to be increased by 1bn manats. This increase is due to debt restructuring of International Bank of Azerbaijan (IBA) (this issue will be analysed in more detail further in the text)[24].

A number of reforms have been envisioned on spending side of the budget. Arguably the most pressing issue facing the policy-makers is the implementation of fiscal rules. Several measures have been taken to increase the transparency and accountability of state enterprises that borrow from abroad with state guarantee. The government also plans to gradually decrease its presence in a number of sectors and to stimulate private investment in these sectors.

Figure 3: Foreign Exchange Reserves (bln. USD)

Figure 3 (a) displays a notable increase in the oil fund reserves in 2017. However, reserves level hasn’t yet returned to its peak level of 2014. On the other hand, as we can see from Figure 3 (b), as the oil prices started to decline in 2014, CBAR reserves dropped sharply. But in 2017, assisted by stabilization of manat, reserves have finally started to rise.

Monetary Policy

In 2017, monetary authority (Central Bank of the Republic of Azerbaijan, CBAR) have continued its preparations for introduction of inflation targeting regime. Although the main policy objective of monetary policy decisions in 2017 have been reduction of inflation, operating regime of CBAR can be characterized as money targeting regime. CBAR has based its main monetary operations around the implementation of monetary program. Tight monetary policy has continued throughout this year. Discount rate is still high (15%) and sterilization operations, which are used to collect excess liquidity of the banks, were further expanded toward the end of the year.

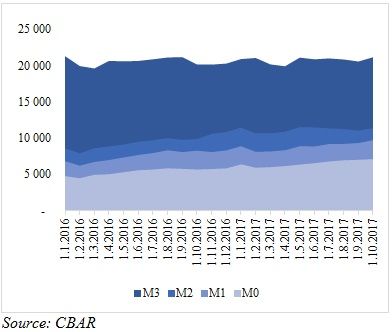

Figure 4: Monetary aggregates

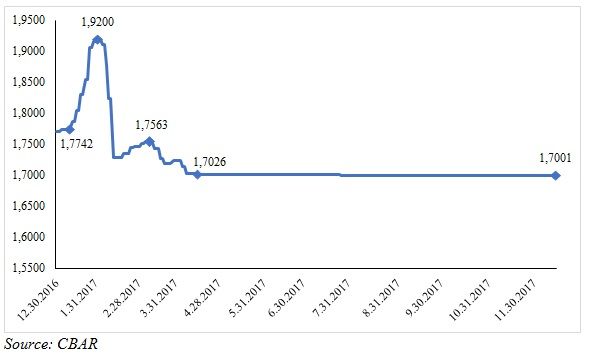

De jure exchange rate regime of the bank has been stated as “managed floating”. Floating regime was introduced in January of 2017[25]. By the end of January, the currency (manat, AZN) has depreciated by 8.4%, from 1.77 to 1.92 AZN/USD. However, in the following months the trend reversed and manat appreciated to 1.70 following market interventions of CBAR through foreign currency auctions. Exchange rate against USD was stable around 1.70 since April (Figure 5). Currency auctions, where the Central Bank sells currency to banks, are carried out twice a week, at a pre-determined amount.

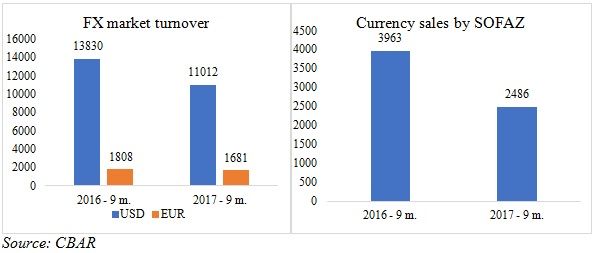

Overall foreign currency demand in the first 9 months of 2017 was 37% lower than the corresponding period of 2016[26]. The volume of USD transactions in the first three quarters of the year have decreased by 20.4% relative to corresponding period of 2016, while euro transactions decreased by 7% (Figure 6). The large majority of operations in currency market were in USD – 83%. It is also interesting to note that sizeable share (95%) of currency transactions in intrabank currency markets (bank’s operations with its customers) was done with legal persons[27]. This implies that, the major part of currency demand in Azerbaijan stems from economic activities of firms, mainly importing. Therefore, we can conclude that, dollarization of private saving has slowed down and the panic surrounding currency market have somehow subsided. This conclusion is further strengthened by the fact that while net cash currency sale of the banks in 2016 (the first three quarters) was 281m USD, while in 2017 it was -117m, i.e. a net purchase[28].

Figure 5: Exchange rate of manat against US dollars in 2017.

Manat was devalued twice in 2015, firstly, from 0.78 to 1.05 in February 2015, then from 1.05 to 1.58 in December. CBAR announced the move toward managed floating regime after the second devaluation. Fluctuations of manat throughout 2016 were minimal, as the bank retained close control of the currency market. In January of 2017 bank also abolished 4% corridor rule (according to this rule, exchange rate difference between buy/sell operations of banks in foreign exchange market and official exchange rate could not exceed 4% in both directions, thus creating a total of 8% corridor around official exchange rate). Understandably, after the abolition of the rule, the spread in foreign exchange market increased sizably, but later it gradually decreased as the exchange rate stabilized (currently, average spread is around 1.5%).

Figure 6: Currency market

In 2016, Financial Stability Board was established. The main objectives of the board are coordination of policy responses of ministries and strengthening of macroeconomic and financial stability. The board includes Assistant to President of the Republic of Azerbaijan on Economic Reforms, the Minister of Finance, the Minister of Economy, Governor of the Central Bank of Azerbaijan, Chairman of the Board of Directors of the Financial Markets Supervisory Authority, Executive Director of the State Oil Fund and is resided by Prime Minister. The board have agreed on monetary program, which specified the target for change in monetary base and its main components. Thus, main policy anchor for monetary policy in 2017 have been monetary base.

Main tools used by CBAR to manage monetary base are sterilization operations. These include deposit auctions and CBAR note emissions. Deposit auctions have started in June 2016. Because of decreased lending, the only relatively risk-free way for banks to employ these excess reserves was the purchase of foreign currencies, which naturally increased the demand in currency auctions and, in turn, put an upward pressure on the exchange-rate. Thus, the main objective of these operations is sterilization of excess liquidity of the banks, decreasing the pressure on manat exchange rate.

CBAR has introduced deposit auctions to present banks an alternative investment opportunity. The interest rate of these deposits varied between lower bound of interest rate corridor and discount rate – 12%-15%. Initially, average interest rate bid by banks hovered around the upper bound (discount rate). However, average interest rate started to decrease after the exchange rate stabilized and the expectations of further depreciation subsided. In June 2017, CBAR has decided to decrease the lower bound of interest rate corridor from 12% to 10%, since the average interest rate in deposit auctions were typically 12.01%[29]. After this reduction, the interest rates have stabilized at 10.01%. Deposit auctions are conducted on a weekly basis and have the maturity of 28 days.

Similar to deposit auctions, CBAR also conducts weekly note auctions. Notes have a maturity of 14 days. Interest rates in these auctions are on the same level as deposit auctions. CBAR prioritizes note auctions as the supply of CBA notes have exceeded the supply in deposit auctions. Currently, total volume of notes in circulation is around 0.7bn AZN.

Overall, increased oil prices have alleviated the panic surrounding the exchange rate of manat, while these sterilization operations have reduced the pressure on the exchange rate in currency auctions.

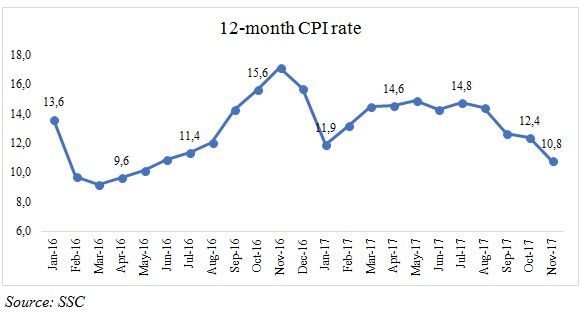

Inflation rate following the devaluation was the foremost problem facing CBAR. Inflation rate reached 15.7% in 2016. However, the effect of depreciation on the price level seems to be waning, as the CPI rate (12-month inflation) have come down to 10.8% in November. Although, this still is higher than CBAR target (which is single-digit inflation), if the trend continues, target might be reached in 2018. According to CBAR, the price of 334 of 593 goods and services have increased, while prices of 94 remained unchanged and 93 have decreased[30].

Main driver of Consumer Price Index (CPI) increase is the increase in the price of food and beverages – 12.9% in the past 12 months. This increase coincides with relative decrease in the global food prices and agricultural prices in general (World Bank). This means that increase in domestic prices is mostly driven by the adjustment process to cheaper manat, rather than international factors. Other contributors to inflation were significant increases in utility prices (price of electricity over certain volume of consumption increased by 55%, while price of natural gas over certain volume increased by 100%). On the other hand, GDP deflator, which reflects price increase of all goods and services produced in the economy, have increased by 18% in the first 3 quarters of 2017[31].

Figure 7: Consumer Price Index

Financial Sector

Difficulties in the banking sector continued in 2017. Although no banks have closed in 2017, the activity in the sector have slowed down noticeably. Lending by banks continued to decline, which is reflected in the decrease in the volume of loan portfolio of the banks. Loan portfolio have decreased by 24.6% by the end of September since the beginning of the year[32]. The decrease is even more stark when compared to the beginning of 2016 – from 21.7bn to 12.4bn manats, a 43.7% decrease. Moreover, the share of non-performing loans is on the rise, while it was 7% in the beginning of 2016, it rose to 9% in the beginning of 2017 and to 15% at the end of September. It also rose in absolute values, from 1.5bn to 1.8bn. Loans to households have decreased the most, which is not surprising considering higher risk associated with these types of loans. These loans have decreased from 8.4bn. to 4.9bn. manats. Furthermore, in line with decreasing activity in construction sector, construction and housing loans have decreased from 3bn to 0.5bn manats[33].

One of the main reasons of large negative effect of devaluation on the welfare of the population and the overall economic activity in Azerbaijan was due to large currency mismatch between the liabilities and income of households and firms. “Currency mismatch” refers to a situation when liabilities and income flows of agents in the economy are denominated in different currencies. Usually, it arises when the agents borrow excessively in foreign currency, expecting the exchange rate to remain stable. This phenomenon is common for many post-Soviet countries.

The dollarization of loans in Azerbaijan was 27% prior to the first devaluation (at the beginning of 2015). By the beginning of 2017 it reached 47.3%. Of 16.4bn of loans, 7.8bn were in foreign currency (which is 4.4bn dollars). By the end of September, it decreased to 42%, while the volume of foreign loans was now 3bn dollars. This is much lower than dollar value of foreign currency loan volume at the beginning of 2015 (which was 5bn manats, or 6.4bn dollars)[34].

The volume of manat deposits have declined significantly in 2015 following the first devaluation, from 7.3bn to around 4.3bn toward the end of the year. However, during 2016 it stabilized around 5bn manats and at the end of September 2017 was 4.9bn. Reasons for this decrease in manat deposits include the fear of further depreciation and the bankruptcy of several large banks. Azerbaijan have deposit insurance scheme, which covered only the deposits less than 30 000 manats. This scheme ensured the return of the funds of the depositors left in the bankrupt bank by the state. But following the large deposit run the limit was temporarily eliminated, now all deposits are covered by the Deposit Insurance Fund. This measure has stabilized the market to certain extent. Interestingly, manat deposits of the households have increased in the analysed period (from 1.5bn to 1.9bn in 2017). However, their dollar deposits have decreased from 5.9bn manats (3.3bn dollars) to 5bn manats (2.9bn dollars)[35]. This may be caused by conversion of dollar deposits into manat deposits, which, in turn, may be caused by the stabilization of manat exchange rate. As we have seen above, panic in the currency market regarding the exchange rate have generally subsided in the past months.

Figure 8: Evolution of bank assets in 2017.

Dollarization of deposits have been higher than that of loans. The volume of dollar deposits has decreased by 0.8bn dollars just in first 9 months of 2017, from 9.4bn to 8.6bn dollars. Dollarization of deposits is currently 74.6%[36]. Although this figure is declining, it is still quite high and poses currency mismatch risks for the banks, since major part of their assets are in manats.

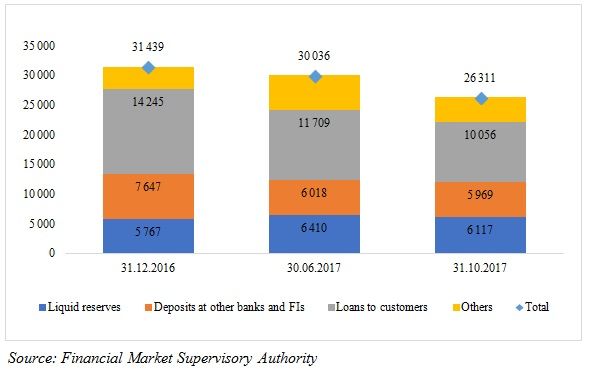

Banking sector predominantly consists of private banks (29 out of 31). There are 16 banks that are partially foreign owned, foreign residents are majority owners of 8 of those. Total assets of the banking sector were equal to 26bn manats at the end of October[37]. The volume of assets has decreased by 16.1% (from 31bn) in 2017. On the other hand, the profitability of the banking sector as a whole has been partially restored: while banks have reported a net loss of 1.6bn manats in 2016 (ROA being -5%), they have reported a net income of 0.5bn in the 10 months of 2017. Although, not all banks have contributed to this increase in total income, majority of small banks still operate at loss. Nevertheless, no bank has failed so far in 2017, which is a welcome change after failures of 5 banks in 2016, one being Bank Standard, third largest bank by the volume of deposits. Deposit Insurance Fund have paid around 0.7bn manats to insured depositors of failed banks during 2017[38].

Concentration of the banking sector is quite high. Top three banks are International Bank of Azerbaijan (IBA), Kapital Bank and Pasha Bank. IBA is a state-owned bank and was the dominant player in the banking sector prior to the difficulties discussed further below. Kapital Bank and Pasha Bank belong to the same parent company. Combined assets of these three banks constitute about 70% of total assets of banking sector[39]. Assets of IBA alone equal to 12bn manats, which is nearly half of the total banking sector.

Baku Stock Exchange (BSE) is relatively underdeveloped. Azerbaijan has yet to have first IPO. Main securities traded in the BSE are CBAR notes and government bonds, which are sold in auctions at a weekly basis. CBAR have increased the volume of its note operations and also their share in total sterilization operations in past months, which can be interpreted as an attempt to facilitate the development of BSE. Maturities of government bonds are 3-month, 6-month, 1 year, 2 years and 3 years. Unlike CBAR notes, there are no interest rate restrictions in government bond auctions. Interest rates in bond auctions have generally been lower than note and deposit auction interest rates. Government bonds sold in BSE are denominated only in manats. One of the most traded securities is SOCAR bonds, which are denominated in dollars. Total volume of securities market has decreased in the first 3 quarters relative to corresponding period of 2016, according to FIMSA[40]. Introduction of CBAR note operations have significantly increased the volume of total government securities, while the volume of corporate securities has decreased. Which can be attributed to crowding-out effect, since the abundance of risk-free, high yield government securities may decrease the attractiveness of corporate securities.

IBA Debt Restructuring

Arguably the most important event in Azerbaijani economy in 2017 was the debt restructuring of International Bank of Azerbaijan. Below we will briefly review the main events leading to restructuring, restructuring process itself and its possible consequences.

Prior to its difficulties, IBA was the largest in the whole South Caucasus region. By 2005 60% of its shares belonged to the state. The bank has participated in a number of major domestic and foreign investment projects. Furthermore, the bank had large loan portfolio and also was a major employer in the economy. Wages of nearly all public employees and pension were (and still are) paid via IBA. More than half of total assets of the banking sector belonged to IBA[41]. Because all of these mentioned facts IBA possessed a systemic importance in the financial sector of economy. Most international observers noted the necessity of the privatization of the bank, which was acknowledged by the authorities, but no concrete steps were taken prior to the crisis.

Economic shock that followed the slump in oil prices have unearthed the fundamental problems of IBA. These included incompetent management, low quality assets and rampant corruption. Chairman of the bank was fired in March and later on he and several other high-ranking managers were imprisoned with charges of fraud, embezzlement and abuse of power[42]. Hajiyev, the former chairman, was found guilty and sentenced to 15 years in jail. The president has decreed the preparation of state-owned assets of the bank for privatization in July of the same year. The losses of the bank amounted to 812m manats in 2015 and 1740m in 2016[43]. These amounts are even more damning when we consider the fact that the net profit in the preceding 14 years amounted to just 355m manats[44].

According to the initial rehabilitation plan, state provided around 11bn manats of liquidity to the bank. This amount was almost 20% of Azerbaijan’s GDP. As a part of this scheme, state relieved IBA of toxic assets via a subsidiary state-owned credit institution (“AqrarKredit”). However, even after the transfer of such a huge share of assets, the volume of non-performing loans increased in 2016 (by 257m manats). Devaluations have seriously weakened currency position of the bank – while 74.5% of bank’s assets were in manat, only 18.6% of its liabilities were manat-denominated[45]. Thus, open currency position of the bank more than tripled relative to the beginning of the year, recording a 4.7bn increase.

In 2016, State Oil Fund of the Republic of Azerbaijan (SOFAZ) made 1bn USD deposit in the bank to provide liquidity[46]. Despite this significant state support, the bank still had problems with paying its foreign liabilities in 2017. On 10th of May 2017 IBA failed to pay the principal and the interest owed on its 100m subordinated debt. The following day the bank announced debt restructuring plan. According to this document, the bank had 3.3bn USD worth of foreign-denominated liabilities (including SOFAZ deposit of 1bn.)[47]. Credit ratings of the bank were immediately lowered to CCC (Fitch) and Caa3 (by Moody’s). The bank approached New York court to ensure that the restructuring process is recognized by USA and to prevent creditors to raise payment demands before the process is fully completed. The court satisfied the bank’s demands and the process was initiated.

The creditors would need to vote on the plan for it to be realized. If the plan would have been voted down, the bank would have defaulted on all of its debts and would probably closed down, which would have been disastrous for the economy of Azerbaijan and its image among potential foreign investors. The plan needed to be approved by the creditors who held at least 2/3rd of all debt to be carried out. Several creditors have expressed their discontent about inclusion of State Oil Fund (which held 1/3rd of all foreign denominated debt of IBA) in the voting process. They argued that, SOFAZ deposited USD 1bn specifically to attend in this vote as a “friendly creditor”[48]. With the vote of 1/3rd of creditors thus ensured, Azerbaijani government now needed to persuade only the half of remaining creditors to get the necessary approval for the restructuring plan. The vote was carried out in July and the plan was approved by the 87% of creditors[49].

According to the plan, further 3.7bn manat toxic assets will be bought by the state. In exchange, 1) government will nationalize 4.0bn manat of foreign liabilities of the bank (this is manat equivalent of non-SOFAZ foreign denominated debt of the bank), 2) it will give the bank 1.1bn in promissory notes, 3) it will increase equity of the bank to 0.6bn (which was previously at -0.7bn manats). As a result, the government will increase the bank’s equity, provide it with promissory notes, relieve it of 4bn manat worth of foreign liabilities and downsize the balance sheet by 21% - from 12.1bn to 9.5bn manats. These operations will improve Tier 1 capital ratio of the bank from negative 9.8% to 13.1%. According to investor presentation presented by the government officials to creditors, these steps will restore the bank’s profitability and also decrease the systemic importance of the bank. Further steps in the plan are disposal of the bank’s subsidiaries in Georgia and Russia (which was planned for 2017) and disposal of state stake in IBA (2018)[50].

The liabilities of the bank are categorized into three groups: trade finance related instruments (USD 861m); senior instruments (USD 2382m, this group includes SOFAZ deposit); subordinated debt (USD 100m). According to the approved plan, 21% of trade finance related instruments will be exchanged for 3-month sovereign debt securities, while 79% would be exchanged for 4-year securities. Three options were presented for senior debt holders: 1) minimum of USD 500m exchanging for 12-year sovereign bonds with 20% haircut (meaning, paying only 80% of the debt’s value); 2) minimum of USD 500m exchanging for 15-year sovereign bonds; and 3) exchanging for 7-year IBA bonds with a maximum amount of USD 1 billion (as was indicated in the investor presentation, this option was “reserved” for the deposit of SOFAZ. Finally, subordinated debt will get a 50% haircut and exchanged for 12-year sovereign bond[51].

Main point of discontent among creditors was the 20% haircut. According to the initial plan, allocation of the senior debt among first two options would be carried out on “first come, first served” principle. If no selection is made by the creditors, their debt would be reallocated equally between two options. This implied that, between 15% to 21% of total foreign liabilities would get a haircut.

As was mentioned before, despite worsening fiscal position, total public debt of Azerbaijan was quite low – 20.5% of GDP. This restructuring plan would see the debt-to-GDP ratio rise by 6 percentage points. The increased level is still considered sustainable and is below mean debt of peer countries[52].

Concluding remarks

The reverberations of oil price slump and subsequent devaluations of national currency were still felt in Azerbaijan throughout 2017. Despite the government’s commitment to diversification, oil and gas retain their vital importance for the economy of the country. Relative increase in the price of oil and planned gas projects mean increased export revenue in the near future, but the growth remains far from sustainable. The SOEs encountered significant challenges following the devaluation of national currency, facing huge financial losses and rising debt levels.

After a period of huge current account surpluses, oil price slump beginning in 2014 have significantly reduced export volume of Azerbaijan, resulting in 2 consecutive years of current account deficit in 2015 and 2016. Although theoretically exchange rate devaluation should have improved current account balance, only the recovery of oil prices has succeeded to improve the CA balance. As a part of diversification efforts, Azerbaijan have been exploring the possibility of developing its largely untapped tourism potential in the past few years.

Transfers from oil fund constituted a significant share of budget revenues in the past years. Dramatic decrease in oil prices have decreased in 2015 by USD 3.5bn, highlighting the significance of diversification of economy and of budget revenues. Fiscal consolidation measures were conducted in 2016 and 2017. While the oil fund transfers have decreased in 2017, consolidation measures have helped to increase customs and tax revenue of the budget. Several measures have been taken to increase the transparency and accountability of state enterprises that borrow from abroad with state guarantee. Implementation of fiscal rules is of great importance, as the increase in the oil price has led to a significant increase in the budget expenditures for 2018.

In 2017, CBAR have continued its preparations for introduction of inflation targeting regime. De jure exchange rate regime of the bank has been stated as “managed floating”, although the actual exchange rate has been stable since April, 2017. Demand for foreign currency has gone down. Overall, increased oil prices have alleviated the panic surrounding the exchange rate of manat, while sterilization operations of CBAR have reduced the pressure on the exchange rate in currency auctions. The effect of depreciation on the price level seems to be waning. If the exchange rate stability persists, the inflation rate is likely to fall to single-digit figures in 2018.

Although a number of measures have been taken to facilitate the recovery of banking sector, there is still great room for future reforms. Difficulties in the banking sector persisted in 2017. Lending by banks continued to decline, while the manat deposits, which decreased significantly after devaluations, were relatively stable. Dollarization of the economy is still quite high, but slowly declining. Successful restructuring of IBA debt have eased the pressure on the financial sector, but increased public debt level. The worst case scenario relating to the bank seems to have been avoided.

[1] Azernews.az. (10.03.2017). “Azerbaijan leaving EITI.” Retrieved from Azernews.az: http://www.azernews.az/business/110036.html.

[2] EITI. (n.d.). “Who we are.” Retrieved from EITI: https://eiti.org/who-weare#implementing-countries

[3] Financial Times, (10.03.2017). “Azerbaijan risks gas pipeline loans by quitting transparency monitor”. Retrieved from Financial Times: https://www.ft.com/content/4fad74e8-056c-11e7- ace0-1ce02ef0def9

[4] Center for Economic & Social Development. “The cost of Azerbaijan’s leaving the Extractive Industries Transparency Initiative (EITI): Analysis of the impact on the economy and civil society”. Retrieved from http://cesd.az/new/wp-content/uploads/2017/03/CESD_EITI_Assessment_Paper.pdf.

[5] Reuters, (14.09.2017) “BP-led group extends Azeri oil 'contract of the century'”. Retrieved from https://www.reuters.com/article/us-bp-azerbaijan-agreement/bp-led-group-extends-azeri-oil-contract-of-the-century-idUSKCN1BP11O.

[6] IMF, “IMF Staff Completes 2017 Article IV Mission to the Republic of Azerbaijan”. Retrieved from http://www.imf.org/en/News/Articles/2017/12/15/pr17498-imf-staff-completes-2017-article-iv-mission-to-the-republic-of-azerbaijan.

[7] Center for Economic & Social Development, “The Current Situation and Problems of State-Owned Enterprises in Azerbaijan”. Retrieved from http://cesd.az/new/wp-content/uploads/2017/12/State-Owned-Enterprises-Azerbaijan.pdf.

[8] Center for Economic & Social Development, “The Current Situation and Problems of State-Owned Enterprises in Azerbaijan”. Retrieved from http://cesd.az/new/wp-content/uploads/2017/12/State-Owned-Enterprises-Azerbaijan.pdf.

[9] Central Bank of the Republic of Azerbaijan, “External Sector Statistics”. Retrieved from https://en.cbar.az/lpages/statistics/external-sector-statistics/.

[10] Customs Committee of the Republic of Azerbaijan, “Trade Statistics”. Retrieved from http://customs.gov.az/en/faydali/gomruk-statistikasi/xarici-ticaretin-veziyyeti-haqqinda/.

[11] Energy Information Agency, “Petroleum and Other Liquids: Spot Prices”. Retrieved from https://www.eia.gov/dnav/pet/pet_pri_spt_s1_d.htm.

[12] Central Bank of the Republic of Azerbaijan, “External Sector Statistics”. Retrieved from https://en.cbar.az/lpages/statistics/external-sector-statistics/.

[13] APA News Agency, (12.10.2017) https://apa.az/turizm_az/nazir-azerbaycana-gelen-turistlerin-sayi-25-faiz-artib-2098.html.

[14] Central Bank of the Republic of Azerbaijan, “External Sector Statistics”. Retrieved from https://en.cbar.az/lpages/statistics/external-sector-statistics/.

[15] Central Bank of the Republic of Azerbaijan, “External Sector Statistics”. Retrieved from https://en.cbar.az/lpages/statistics/external-sector-statistics/.

[16] State Oil Fund of the Republic of Azerbaijan, “Annual Report, 2016”. Retrieved from http://www.oilfund.az/uploads/Annual_Report_2016_ENG.pdf.

[17] State Oil Fund of the Republic of Azerbaijan, “SOFAZ revenue and expenditure Statement for January-September 2017”. Retrieved from http://www.oilfund.az/en_US/hesabat-arxivi/rublukh/2017_1/2017_1_3/

[18] Ministry of Finance, “Budget Presentation, 2017”. Retrieved from http://maliyye.gov.az/sites/default/files/Budce-16-11-2016.pdf.

[19] Ministry of Finance, “Budget Presentation, 2017”. Retrieved from http://maliyye.gov.az/sites/default/files/Budce-16-11-2016.pdf.

[20] Ministry of Finance, “Budget Presentation, 2017”. Retrieved from http://maliyye.gov.az/sites/default/files/Budce-16-11-2016.pdf.

[21] Ministry of Finance, “Information (operative) on the execution of the state budget for nine months of 2017”. Retrieved from http://www.maliyye.gov.az/en/node/2087.

[22] Ministry of Finance, “Budget Presentation, 2017”. Retrieved from http://maliyye.gov.az/sites/default/files/Budce-16-11-2016.pdf.

[23] Ministry of Finance, “Budget Presentation, 2017”. Retrieved from http://maliyye.gov.az/sites/default/files/Budce-16-11-2016.pdf.

[24] Ministry of Finance, “Milli Majlis approves amendments to the state budget for 2017”. Retrieved from http://www.maliyye.gov.az/en/node/2061

[25] Reuters, (12.01.2017) “Azerbaijan drops FX rate corridor to float manat currency”. Retrieved from https://www.reuters.com/article/azerbaijan-forex/update-1-azerbaijan-drops-fx-rate-corridor-to-float-manat-currency-c-bank-idUSL5N1F23R1.

[26] Central Bank of the Republic of Azerbaijan, Monetary Policy Review: III Quarter 2017.

[27] Central Bank of the Republic of Azerbaijan, Monetary Policy Review: III Quarter 2017.

[28] Central Bank of the Republic of Azerbaijan, Monetary Policy Review: III Quarter 2017.

[29] Central Bank of the Republic of Azerbaijan, “Press-release on changes to parameters of interest rate corridor”. Retrieved from https://en.cbar.az/releases/2017/06/22/press-release-on-changes-to-parameters-of-interest-rate-corridor/.

[30] Central Bank of the Republic of Azerbaijan, Monetary Policy Review: III Quarter 2017.

[31] State Statistical Committee, “Price and Tariff Indexes”. Retrieved from https://www.stat.gov.az/source/price_tarif/?lang=en.

[32] Central Bank of the Republic of Azerbaijan, “Electronic Statistics Base”. http://esasodi.cbar.az:9704/obiee/ESAHS.jsp.

[33] Central Bank of the Republic of Azerbaijan, “Electronic Statistics Base”. http://esasodi.cbar.az:9704/obiee/ESAHS.jsp.

[34] Central Bank of the Republic of Azerbaijan, “Electronic Statistics Base”. http://esasodi.cbar.az:9704/obiee/ESAHS.jsp.

[35] Central Bank of the Republic of Azerbaijan, “Electronic Statistics Base”. http://esasodi.cbar.az:9704/obiee/ESAHS.jsp.

[36] Central Bank of the Republic of Azerbaijan, “Electronic Statistics Base”. http://esasodi.cbar.az:9704/obiee/ESAHS.jsp.

[37] Financial Market Supervisory Authority, “Banking Sector Main Statistics”. Retrieved from https://www.fimsa.az/en/statistika.

[38] Azerbaijan Deposit Insurance Fund, Press Release, (08.12.2017). Retrieved from http://adif.az/?~/aze/news/full/1/1136/.

[39] Kapital Bank, “III Quarter Balance Sheet, 2017”. Retrieved from https://kapitalbank.az/useruploads/reports/Balans_hesabati_ENG.pdf.

Pasha Bank, “III Quarter Balance Sheet, 2017”. Retrieved from https://www.pashabank.az/about_us/uploads/hesabat/2017_10/Financial_Reports_III_quarter_2017.pdf.

[40] Financial Market Supervisory Authority, “Securities Market Statistics”. Retrieved from https://www.fimsa.az/en/statistics.

[41] International Bank of Azerbaijan, “Reliable Report 2005”. Retrieved from

https://www.ibar.az/site/assets/files/1651/abb_illik_hesabat_2005.pdf.

[42] Trend News Agency, (14.10.2016) "Jahangir Hajiyev was sentenced to 15 years in prison (UPDATED-2)". Retrieved from https://az.trend.az/azerbaijan/society/2670999.html.

[43] International Bank of Azerbaijan, (11.05.2017) “International Bank of Azerbaijan the next stage of the recovery process begins”, Retrieved from https://www.ibar.az/en/investors/debt-restructuring/press-releases/#11.05.2017.

[44] Center for Economic and Social Development, “International Bank of Azerbaijan: Why the South Caucasus's largest bank has requested restructuring?” Retrieved from http://cesd.az/new/wp-content/uploads/2017/08/CESD_Research_Paper_International_Bank_Azerbaijan.pdf.

[45] Center for Economic and Social Development, “International Bank of Azerbaijan: Why the South Caucasus's largest bank has requested restructuring?” Retrieved from http://cesd.az/new/wp-content/uploads/2017/08/CESD_Research_Paper_International_Bank_Azerbaijan.pdf.

[46] State Oil Fund of the Republic of Azerbaijan, “Annual Report – 2016”, Retrieved from http://www.oilfund.az/uploads/Annual_Report_2016_ENG.pdf.

[47] International Bank of Azerbaijan, “Indicative Restructuring Plan”. Retrieved from https://www.ibar.az/site/assets/files/5800/restructuring_plan_english-1.pdf.

[48] Bloomberg, (23.05.2017) “Creditors Cry Foul After Default as Azeri Bank Offers Debt Swap”. Retrieved from https://www.bloomberg.com/news/articles/2017-05-23/defaulted-azeri-bank-offers-swap-into-sovereign-debt-new-bonds.

[49] Bloomberg, (12.07.2017). “Defaulted Azerbaijan Bank Wins Approval for Debt Restructuring Plan”, Retrieved from https://www.bloomberg.com/news/articles/2017-07-12/defaulted-azeri-lender-wins-creditor-backing-for-debt-overhaul.

[50] International Bank of Azerbaijan, “Investor Presentation”. Retrieved from https://www.ibar.az/site/assets/files/3434/20170523_-_iba_investor_presentation_vf.pdf.

[51] International Bank of Azerbaijan, “Investor Presentation”. Retrieved from https://www.ibar.az/site/assets/files/3434/20170523_-_iba_investor_presentation_vf.pdf.

[52] International Bank of Azerbaijan, “Investor Presentation”. Retrieved from https://www.ibar.az/site/assets/files/3434/20170523_-_iba_investor_presentation_vf.pdf.

|

|

НАСТРОЕНИЯ В АРМЯНСКОМ ОБЩЕСТВЕ КАК ПРЕДВЕСТНИК БУДУЩИХ ИЗМЕНЕНИЙ | Степан Григорян |

БЕЛАРУСЬ: В ОЖИДАНИИ СЛОЖНОГО ГОДА | Игорь Тышкевич |

|